Written by: Segun Akomolafe

Let’s be real — many people don’t have an idea of how to create a personal financial plan that actually works for their life. You hear terms like budgeting, investing, and net worth, and somehow they all feel like things other people do. But here’s the truth: without a clear financial plan, you’re essentially driving without a map. You might get somewhere eventually, but you’re going to burn a lot of fuel getting there.

A solid personal financial plan isn’t about restriction or complicated spreadsheets. It’s about knowing where you stand, deciding where you want to go, and mapping out the specific steps to get there. Whether you’re 22 and just starting out or 45 and playing catch-up, the process works the same way. Let’s break it down — step by step.

What Is a Personal Financial Plan — And Why Does It Actually Matter?

A personal financial plan is a written strategy that covers your income, expenses, savings goals, investments, insurance, debt repayment, and long-term wealth targets — all in one place. Think of it as a financial GPS. It doesn’t tell you what you can’t do; it shows you what’s possible and how to get there.

Here’s the part most financial advice skips: it matters because of what happens when you don’t have one. People without a plan consistently overspend, under-save, and reach their 50s wondering why retirement feels so far away. According to the Federal Reserve, nearly 40% of American adults can’t cover a $400 emergency without borrowing. That’s not an income problem — it’s a planning problem.

Knowing how to create a personal financial plan gives you a framework to make smarter decisions automatically. You stop reacting to money and start directing it.

Read More: Basic Financial Concepts You Should Understand

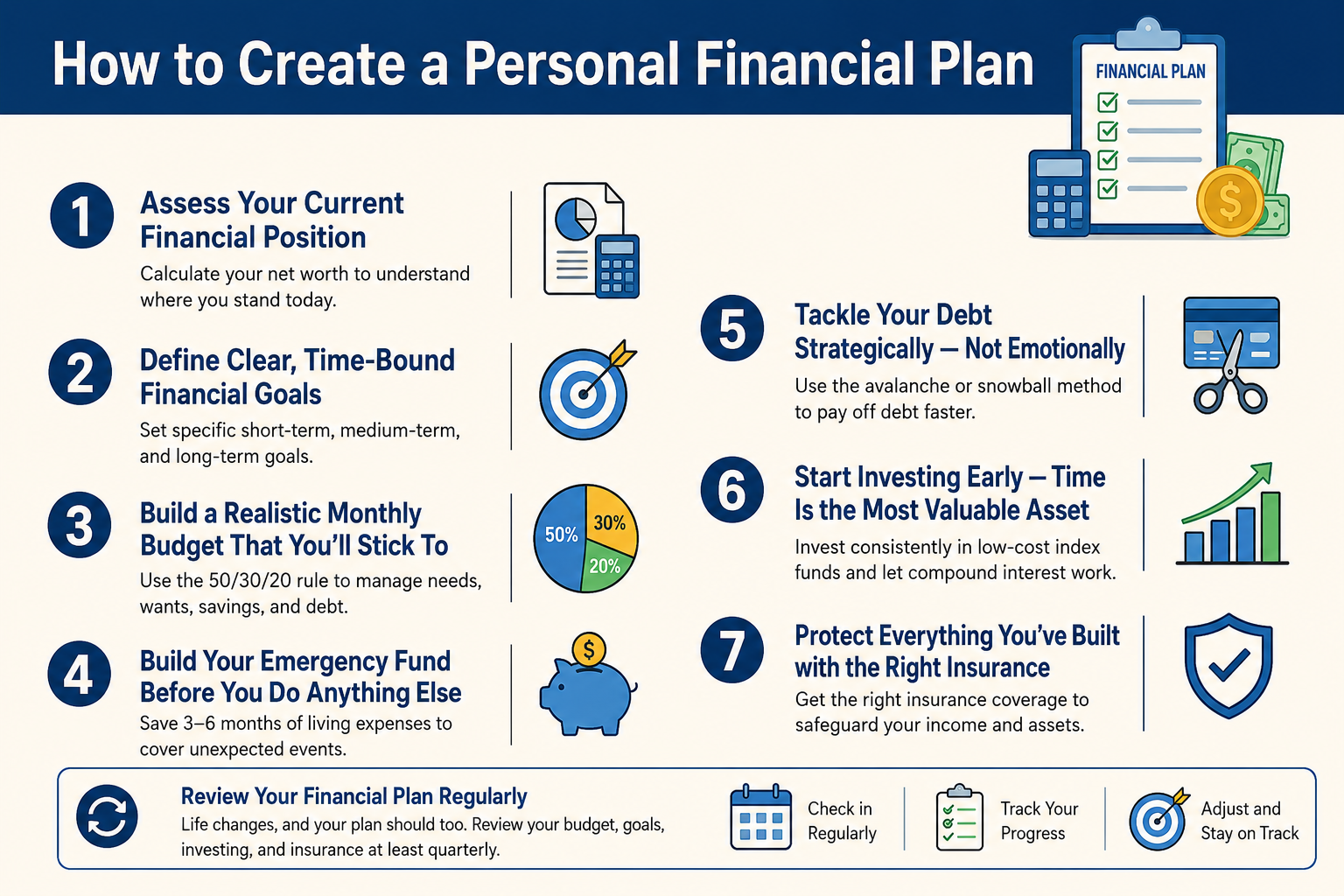

Step 1: Assess Your Current Financial Position

You can’t plan a route if you don’t know where you’re starting from. Before anything else, you need an honest picture of your finances right now. That means calculating your net worth — the difference between everything you own and everything you owe.

Add up your assets: checking and savings accounts, retirement accounts, real estate equity, car value, investments. Then list your liabilities: credit card debt, student loans, car loans, mortgage balance, and any other money you owe. Subtract your total liabilities from your total assets, and that number — positive or negative — is your net worth today.

Don’t panic if it’s negative. A lot of people learning how to create a personal financial plan for the first time discover they’re in the red. That’s what the plan is for.

Table 1: Net Worth Assessment Snapshot

Category | Examples | Your Estimate |

|---|---|---|

Assets — Liquid | Checking, savings, cash | $______ |

Assets — Investment | 401(k), IRA, stocks, crypto | $______ |

Assets — Property | Home equity, car value | $______ |

Liabilities — Short-term | Credit cards, personal loans | $______ |

Liabilities — Long-term | Mortgage, student loans, auto loan | $______ |

Net Worth (Assets − Liabilities) | — | $______ |

Read More: Reserve Fund vs. Savings Account: What’s the Difference?

Step 2: Define Clear, Time-Bound Financial Goals

Vague goals are the enemy of financial progress. “Save more money” is not a goal — it’s a wish. A real financial goal sounds like this: “Build a $10,000 emergency fund by June 2027” or “Pay off $6,500 in credit card debt within 18 months.” The specificity is what makes it actionable.

When you’re figuring out how to create a personal financial plan, it helps to break goals into three time horizons:

- Short-term (0–2 years): Build an emergency fund, pay off high-interest debt, save for a vacation or car repair fund.

- Medium-term (2–7 years): Save for a home down payment, pay down student loans, fund a business idea, or build a 6-month expense buffer.

- Long-term (7+ years): Retirement savings, funding a child’s education, building generational wealth, or achieving financial independence.

Write these goals down. Seriously — put pen to paper or open a notes app right now. Research consistently shows that people who write their financial goals down are significantly more likely to achieve them than those who just think about them.

Read More: 7 Smart Savings Tips Everyone Should Know

Step 3: Build a Realistic Monthly Budget That You’ll Actually Stick To

Here’s where most personal financial plans fall apart — the budget. People create unrealistic spending targets, last three weeks, then give up entirely. The trick is building a budget that reflects your real life, not an idealized version of it.

Start with your actual after-tax income. Then track your real spending from the last 30 to 60 days — not what you think you spend, but what you actually spent. Most people are genuinely surprised. A Starbucks habit and a handful of streaming subscriptions can easily add up to $250 a month you didn’t consciously account for.

The 50/30/20 rule is an excellent starting framework for anyone who’s learning how to create a personal financial plan. Here’s what it looks like:

- 50% toward needs: Rent, groceries, utilities, transportation, insurance, minimum debt payments.

- 30% toward wants: Dining out, entertainment, travel, hobbies, subscriptions.

- 20% toward savings and debt repayment: Emergency fund, retirement contributions, paying down debt faster than required.

The 20% slice is your real financial growth engine. If your take-home is $4,000 a month, that’s $800 working for your future every single month — $9,600 a year. Automate it on payday so it moves before you get a chance to spend it.

Table 2: 50/30/20 Budget Breakdown by Monthly Income

Monthly Take-Home | Needs (50%) | Wants (30%) | Savings/Debt (20%) |

|---|---|---|---|

$2,000 | $1,000 | $600 | $400 |

$3,500 | $1,750 | $1,050 | $700 |

$5,000 | $2,500 | $1,500 | $1,000 |

$7,500 | $3,750 | $2,250 | $1,500 |

$10,000 | $5,000 | $3,000 | $2,000 |

Read More: How to Create a Debt-Free Budget: 5 Key Strategies

Step 4: Build Your Emergency Fund Before You Do Anything Else

Before you put a single extra dollar into investments or debt payoff, you need a financial cushion. An emergency fund is the difference between a minor inconvenience and a full-blown financial crisis. Car breaks down? Medical bill shows up? Job gone? With three to six months of living expenses in a liquid savings account, those events become manageable, not catastrophic.

Start with a $1,000 starter emergency fund if you’re starting from scratch. Get that in place first. Then build to your full target — typically three months of expenses for dual-income households, and six months for single-income or self-employed individuals. Keep it in a high-yield savings account where it earns interest but stays accessible.

Here’s the honest drawback people don’t mention: keeping six months of expenses in cash can feel wasteful when inflation is running hot. And it is, slightly. But the stability it gives you — the ability to take a calculated career risk, to weather a health crisis without debt — is worth far more than the 1–2% you’re giving up by not investing it.

Step 5: Tackle Your Debt Strategically — Not Emotionally

Debt is the single biggest drag on most people’s financial plans. High-interest debt, especially credit card balances at 18–24% APR, actively destroys wealth. Every month you carry a $5,000 credit card balance at 22% APR, you’re burning about $92 in interest — money that goes nowhere for you.

There are two proven strategies for paying down debt, and neither one is wrong — it’s about which one you’ll actually use:

- Debt Avalanche: Pay minimum balances on all debts, then throw every extra dollar at the highest-interest rate debt first. This is mathematically optimal — you pay less total interest over time.

- Debt Snowball: Pay minimum balances everywhere, but attack the smallest balance first for quick wins. This is psychologically powerful — early momentum keeps you motivated.

- Debt Consolidation: Consider consolidating multiple high-interest debts into a single lower-rate personal loan if your credit score qualifies. This simplifies payments and can meaningfully reduce interest costs.

The real key in any solid financial plan is sequencing your debt payoff correctly. Start with your $1,000 emergency starter fund, then attack high-interest debt aggressively, then complete your full emergency fund. Once debt is cleared, redirect every freed-up payment straight into savings and investment.

Read More: Debt Snowball vs Avalanche Method: Which Pays off Debt Faster?

Step 6: Start Investing Early — Time Is the Most Valuable Asset You Have

Once your emergency fund is solid and high-interest debt is handled, it’s time to put your money to work. Investing is where how to create a personal financial plan gets genuinely exciting — because compound interest is one of the few places in finance where the math is unambiguously on your side.

Start with tax-advantaged accounts. If your employer offers a 401(k) match, contribute at least enough to get the full match — it’s a 50–100% instant return that no investment beats. Then max out a Roth IRA if you’re eligible ($7,000 in 2025 for those under 50). After that, invest in a taxable brokerage account using low-cost index funds like S&P 500 ETFs.

Here’s the honest truth about investing: it feels boring. Index funds aren’t thrilling. But the average annual return of the S&P 500 over the last 30 years has been roughly 10–11% before inflation. A $500 monthly investment at that rate for 30 years grows to over $1.1 million. You don’t need a hot stock tip. You need consistency and time.

Step 7: Protect Everything You’ve Built with the Right Insurance Coverage

A good personal financial plan doesn’t just grow wealth — it protects it. Insurance is a critical shield between your financial progress and a catastrophic setback. One serious illness, one at-fault accident, or one month of unexpected disability can wipe out years of savings if you’re underinsured.

At minimum, you should have health insurance, auto insurance, renter’s or homeowner’s insurance, and term life insurance if anyone depends on your income. If you’re self-employed or your income is commission-based, add short-term and long-term disability coverage to that list.

Review your coverage annually — especially after major life changes like marriage, having children, buying a home, or a significant income increase. The goal is to have enough coverage that a major life event doesn’t require you to drain your savings or go into debt.

Step 8: Review Your Financial Plan Regularly — Life Changes, Plans Should Too

The biggest mistake people make after learning how to create a personal financial plan is treating it like a one-time event. Your plan should be a living document. Life changes — your income goes up, you have a child, you get married, you change careers, the market shifts. Your plan needs to keep up.

Set a calendar reminder for a quarterly financial check-in. Spend 30–60 minutes reviewing your budget, tracking your net worth progress, assessing your investment performance, and checking whether your goals still reflect your current priorities. Once a year, do a deeper annual review — adjust insurance coverage, rebalance your investment portfolio, and revisit your long-term targets.

The most financially successful people aren’t the ones with the best plan on day one. They’re the ones who keep showing up, adjusting when needed, and staying consistent through the ups and downs. That’s how to create a personal financial plan that actually works — not as a perfect document, but as an evolving strategy that grows with you.

Table 3: Personal Financial Plan — Monthly Review Checklist

Review Area | What to Check | Frequency |

|---|---|---|

Budget vs. Actuals | Compare planned spending to real spending by category | Monthly |

Net Worth Tracking | Update asset and liability totals; note changes | Monthly |

Confirm balance; replenish if used | Monthly | |

Debt Progress | Track remaining balances; confirm payoff timeline | Monthly |

Investment Contributions | Confirm auto-contributions ran; check allocations | Monthly |

Insurance Coverage | Review policies; adjust for life changes | Annually |

Goal Progress | Measure progress toward short, medium, long-term goals | Quarterly |

Tax Planning | Review contribution limits, deductions, estimated taxes | Annually |

Common Mistakes People Make with Personal Financial Plans

Let’s be honest about what actually derails financial plans — because knowing the pitfalls is half the battle.

- Skipping the emergency fund: People jump straight into investing and then pull money out at a loss the moment an unexpected expense hits. Build the financial buffer first, always.

- Setting unrealistic timelines: Paying off $30,000 of student debt in 12 months on a $45,000 salary isn’t a plan — it’s a setup for failure and burnout. Be ambitious but honest.

- Treating the plan as permanent: Plans that aren’t revisited become obsolete. A financial plan from 2020 doesn’t account for a 2024 salary increase or a new baby.

- Focusing only on saving, ignoring investing: Saving is essential. But money sitting in a 0.5% savings account while inflation runs at 3–4% is quietly losing value every year. Both matter.

- Waiting for the “right time” to start: There is no perfect moment. The best time to learn how to create a personal financial plan was five years ago. The second best time is today.

Read More: How to Pay Off Your Most Important Bills First: A Step-by-Step Priority Guide

The Best Tools to Help You Build and Track Your Financial Plan

You don’t need to do this with a pencil and yellow legal pad (though you absolutely can). There are some genuinely great tools that make building and maintaining a personal financial plan much easier:

- YNAB (You Need A Budget): Best for people who want to zero-base their budget and assign every dollar a job. Steep learning curve, powerful results.

- Mint or Monarch Money: Great for automatic spending tracking and budget visibility across all your accounts in one dashboard.

- Personal Capital (Empower): Excellent for net worth tracking and investment portfolio monitoring alongside budgeting.

- A simple spreadsheet: Google Sheets or Excel still work beautifully. Build your own budget and net worth tracker with full transparency into every formula.

- High-yield savings accounts: SoFi, Marcus by Goldman Sachs, and Ally Bank currently offer competitive APYs — keep your emergency fund and sinking funds here.

Frequently Asked Questions

Still got questions? Here are simple answers to the most valuable questions people ask on how to create a personal financial plan.

How long does it take to create a personal financial plan?

A basic personal financial plan can be built in a few focused hours. Set aside one weekend to assess your net worth, list your goals, and sketch a budget. Refinement takes a few weeks.

Do I need a financial advisor to create a personal financial plan?

No — most people can build a solid plan independently. A fee-only financial advisor adds value for complex situations like estate planning, tax optimization, or managing a significant inheritance.

What’s the most important step when learning how to create a personal financial plan?

Starting is the first and most important step. Most people overthink the process. Write down your current income, expenses, and one financial goal today. That simple first step outweighs any perfect plan never executed.

Related Contents:

- How to Create a Debt-Free Budget: 5 Key Strategies

- 7 Smart Savings Tips Everyone Should Know

- Debt Snowball vs. Avalanche Method: Which Pays Off Debt Faster?

- How to Pay Off Your Most Important Bills First: A Step-by-Step Priority Guide

- How to Invest Early: 7 Strategies for Better ROI

- How Much Money Should You Really Save to Build Financial Security?

- How to Live Within Your Means

- Basic Financial Concepts You Should Understand

- Reserve Fund vs. Savings Account: What’s the Difference?

- Best Budgeting Apps for Managing Your Funds