Written by: Segun Akomolafe

Your credit utilization ratio is one of the most influential factors affecting your credit score. At 30% of your FICO score calculation, it carries significant weight in determining your financial reputation. Yet many people overlook this powerful lever for credit improvement. This article covers some valuable tips on how to improve your credit utilization ratio.

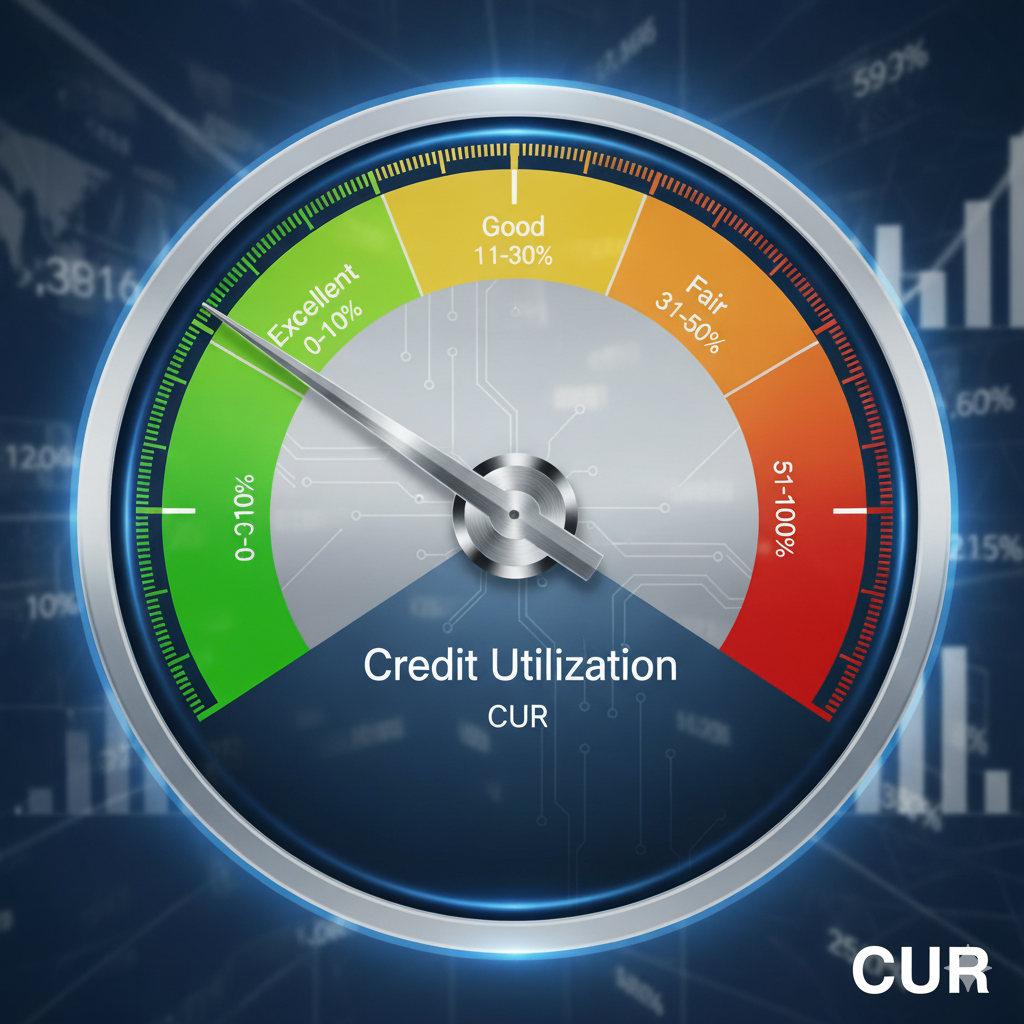

What Is Credit Utilization Ratio?

Your credit utilization ratio represents the percentage of your available credit that you’re currently using. For example, if you have credit cards with combined limits of $10,000 and carry balances totaling $3,000, your utilization ratio is 30%.

This ratio matters to lenders because it indicates how you manage revolving credit. High utilization suggests you might be financially stretched, while lower utilization signals responsible credit management.

Why Your Credit Utilization Ratio Matters

Lenders and credit bureaus view high utilization as a risk factor. Research shows that consumers using more than 30% of their available credit are statistically more likely to miss payments or default on obligations. When your ratio creeps above this threshold, your credit score typically begins to decline—sometimes significantly.

The good news? Unlike negative marks that can linger for years, your utilization ratio has no memory. Reduce it today, and your score can improve next month when new balances are reported.

The Ideal Credit Utilization Target

Financial experts generally recommend keeping your utilization below 30% for decent credit scores. However, if you’re aiming for excellent credit (800+), you’ll want to target under 10%. Those with the highest credit scores typically maintain utilization ratios between 1-7%.

Remember that utilization matters in two ways:

- Per-card utilization: The percentage used on each individual credit card

- Overall utilization: The total across all your revolving accounts

Both metrics impact your score, so pay attention to individual cards with high balances, even if your overall ratio looks reasonable.

13 Effective Strategies to Improve Your Credit Utilization Ratio

Here are the most effective strategies on how to improve your credit utilization ratio:

1. Pay Down Your Balances

The most straightforward approach on how to improve your credit utilization ratio is to reduce your existing debt. Start by targeting high-interest cards first to save money while improving your utilization. Even small additional payments can make a meaningful difference.

Consider this: If you have a $5,000 limit card with a $2,500 balance (50% utilization), paying down just $500 drops your utilization to 40%—potentially boosting your score by several points.

2. Make Multiple Payments Throughout the Month

Credit card issuers typically report your balance to credit bureaus once monthly, usually on your statement closing date. If you make a large purchase and wait for your regular payment due date, that high balance gets reported even if you pay in full later.

By making multiple smaller payments throughout the month, you can keep your reported balance lower. This strategy works particularly well if you use credit cards for everyday expenses or large purchases.

3. Request Credit Limit Increases

Another important strategy on how to improve your credit utilization ratio is to request credit limit increase. The point is that Increasing your available credit immediately improves your utilization ratio, assuming your spending remains the same. Many issuers allow you to request limit increases online or through their app without triggering a hard credit inquiry.

Before requesting an increase, ensure your account has been open for at least 6-12 months with a history of on-time payments. Most issuers automatically review accounts for increases periodically, but being proactive can accelerate the process.

Read more: Savings Vs. Investing: Which One Should You Choose?

4. Apply for a New Credit Card

Opening a new credit card increases your total available credit, thereby improving your overall utilization ratio. This strategy works best if you:

- Have good enough credit to qualify for desirable terms

- Don’t plan major financing (like a mortgage) in the next 6-12 months

- Can resist using the new credit for additional spending

The temporary ding from the credit inquiry and new account is typically offset by the improved utilization ratio within a few months.

5. Keep Old Accounts Open

That old credit card you rarely use? It’s helping your credit score by contributing to your available credit. Closing accounts reduces your total credit limit and can increase your utilization ratio overnight.

If an unused card carries an annual fee, call the issuer to see if they’ll waive it or downgrade to a no-fee version before closing the account.

6. Use Balance Transfers Strategically

Balance transfer offers can consolidate debt onto a card with 0% interest, saving money while you pay down balances. However, these transfers often incur fees (typically 3-5% of the transferred amount).

This strategy makes sense when:

- You qualify for a card with sufficient transfer limit

- The fee is less than what you’d pay in interest

- You have a plan to pay down the balance during the promotional period

Remember that maxing out a new card with a balance transfer creates 100% utilization on that account, so the ideal approach combines a transfer with some additional available credit.

7. Time Your Payments With Statement Closing Dates

Your credit card balance is typically reported to credit bureaus on your statement closing date, not your payment due date. By making payments before this date, you can ensure a lower balance gets reported.

Call your credit card companies to confirm exactly when they report to bureaus, then schedule payments accordingly. Even if you can’t pay in full, reducing the balance before reporting occurs can improve your utilization ratio.

Read more: 15 Best Online Banks For Reliable Savings

8. Ask for “Goodwill” Adjustments

If you’ve occasionally carried a higher balance but are otherwise a good customer, some issuers will make a one-time courtesy adjustment to your credit limit or adjust when they report your balance.

This strategy works best if you have a specific reason (like a temporary emergency expense) and a history of responsible account management.

9. Consider a Personal Loan for Debt Consolidation

Unlike credit cards, installment loans don’t factor into your utilization ratio. By consolidating credit card debt with a personal loan, you can simultaneously:

- Reduce your utilization ratio to zero on those accounts

- Potentially secure a lower interest rate

- Create a fixed repayment schedule

This approach can provide a significant credit score boost while simplifying your debt management. However, it’s crucial not to see newly cleared credit cards as an invitation to spend more.

10. Monitor All Your Credit Card Statement Dates

Different cards report to the bureaus at different times of the month. By understanding this schedule, you can strategically time large purchases to minimize their impact on your utilization.

For example, if you need to make a $2,000 purchase, doing so on a card that just reported to the bureaus gives you nearly a month to pay it down before it affects your credit utilization.

11. Request Credit Reporting Updates

After paying down significant balances, you can request that your credit card company report your new balance to the credit bureaus ahead of the regular schedule. Not all issuers will accommodate this request, but some will—particularly if you’ve been a loyal customer.

This can accelerate the positive impact on your credit score rather than waiting for the next reporting cycle.

12. Utilize Secured Credit Cards

If you’re rebuilding credit or struggling to qualify for limit increases, secured credit cards can help. These cards require a security deposit that typically becomes your credit limit.

By managing a secured card responsibly and keeping utilization low, you demonstrate creditworthiness while building a positive history that can lead to unsecured cards with higher limits.

13. Set Up Utilization Alerts

Many credit card issuers and credit monitoring services allow you to set alerts when your utilization exceeds a certain threshold. Now, the question here is “how to improve your credit utilization ratio with utilization alerts.” The simple answer is that you should set utilization alerts at 20% or 25% to give yourself time to make payments before crossing the 30% mark.

Read more: 20 Tips For First-Time Home Buyers

Maintaining Low Utilization Long-Term

Improving your utilization ratio isn’t just about quick fixes—it requires sustainable habits. Here’s how to maintain healthy utilization:

Create a Spending Plan

Track your expenses to understand your typical monthly credit card usage. Then determine what percentage of your credit limits this represents and adjust your habits accordingly.

Consider setting personal limits below your actual credit limits. For example, if your card has a $5,000 limit, mentally treat it as $1,500 to stay under 30% utilization.

Automate Minimum Payments

Set up automatic minimum payments on all your credit cards to prevent late fees and penalties if you forget a payment. Then make additional manual payments to reduce balances further.

This safety net ensures you never miss a payment due date while giving you flexibility in how aggressively you pay down balances.

Regular Credit Monitoring

Check your credit reports at least quarterly to track your progress and catch any reporting errors. Many credit cards now offer free FICO score access, making it easier than ever to monitor the impact of your utilization improvements.

Read more: Best Bank Bonuses And Promotions in the US

When Higher Utilization Might Be Temporary

Sometimes life happens—medical emergencies, essential home repairs, or periods between jobs can lead to higher credit utilization. If you find yourself in this situation:

- Communicate with your creditors about hardship programs

- Create a realistic debt reduction plan once the crisis passes

- Consider whether a personal loan might provide better terms

- Focus on making at least minimum payments on time

Remember that utilization has no memory, so once you reduce those balances, your score can recover relatively quickly.

Final Thoughts

Your credit utilization ratio is one of the few credit factors you can influence quickly. By implementing these strategies, you can see meaningful improvements in your credit score in as little as 30-60 days.

The best approach combines immediate tactical moves (like paying down balances and requesting limit increases) with long-term habits that keep your utilization low. This balanced strategy not only improves your credit score but also establishes a foundation for lasting financial health.

Ultimately, managing your credit utilization isn’t just about achieving a higher credit score—it’s about creating financial flexibility and peace of mind in a world where credit access increasingly determines your options.

Related Contents: