Written by: Segun Akomolafe

Managing a large number of bills and unsure of which to pay first? It’s crucial to figure out how to pay your bills wisely. Knowing what to pay first can help you stay on track and avoid debt, late fees, and bad credit when money is tight.

This helpful guide will demonstrate how to prioritize your bills, pay for necessities, and create a payment schedule that suits you. These detailed instructions will help you handle your bills with confidence, whether you’re going through a difficult time or simply trying to get your finances in order for the long term.

Learning About Bill Priorities

Not every bill is made equally. You must comprehend the four main payment categories in order to learn how to effectively handle your bills. Depending on how they impact your daily life and future financial situation, your must-pay bills are divided into several categories. The bills that keep you safe and secure are known as Tier 1 bills.

These include housing payments that provide you with a place to live, utilities that guarantee you have a basic standard of living, food expenses, and transportation costs that support your income. These are the most important since failing to pay them could result in major issues. Rent arrears can result in eviction, and power outages during inclement weather can be hazardous.

| Priority Tier | Bill Types | Consequence of Non-Payment |

|---|---|---|

| Tier 1 | Rent/Mortgage, Utilities, Food, Essential Transportation | Eviction, service disconnection, hunger, loss of income |

| Tier 2 | Secured Debts, Insurance, Child Support | Repossession, legal action, loss of protection |

| Tier 3 | Student Loans, Medical Bills, Credit Cards | Credit damage, collection calls, wage garnishment |

| Tier 4 | Subscriptions, Memberships, Discretionary Services | Service cancellation, minor inconvenience |

Read more: Debt Snowball vs. Avalanche Method: Which Pays Off Debt Faster?

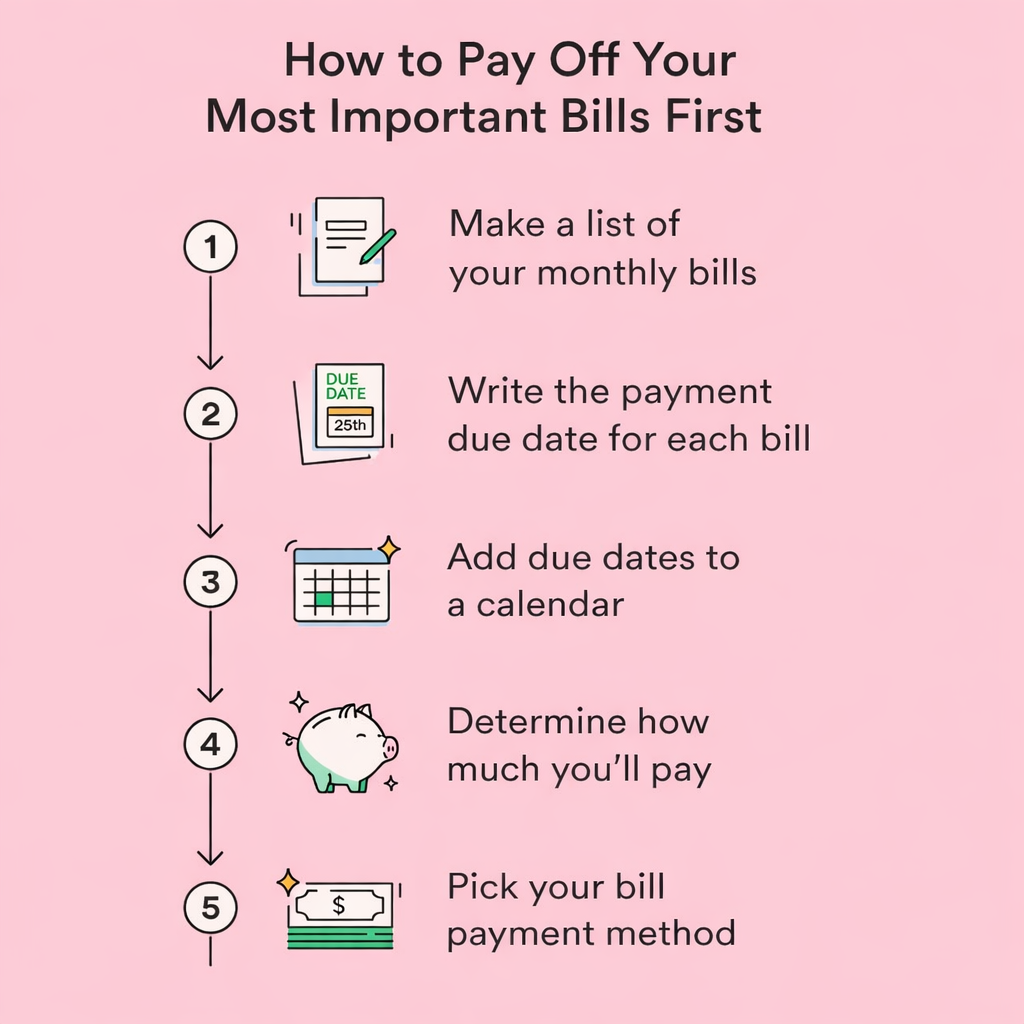

Creating Your Priority Debt List

Your priority debt list becomes your financial roadmap during challenging times. Start by listing every monthly obligation you have, from the mortgage down to streaming subscriptions. For each bill, document the amount due, due date, and consequences of late payment. This comprehensive inventory reveals the complete picture of which bills to pay first based on your unique situation.

Next, assign each bill to its appropriate tier using the framework above. Some bills may seem to straddle categories. For example, a car payment could be Tier 1 if you need the vehicle for work, or Tier 2 if you have alternative transportation. Context matters.

Consider your specific circumstances when making these determinations. Don’t wait for money to arrive in your checking account. To avoid the temptation to spend money, use HR tools to automatically allocate a portion of your direct deposit to a debt payment.

Essential Bills You Must Never Skip

Certain bills demand payment regardless of your budget or financial situation. Understanding how to pay off bills starts with protecting these non-negotiables:

- Housing costs (rent or mortgage) to prevent eviction or foreclosure proceedings that can devastate your living situation and credit for years

- Essential utilities like water, heat, and electricity that maintain safe living conditions and prevent dangerous disconnections

- Minimum food budget that ensures adequate nutrition for your household without relying on emergency assistance

- Transportation expenses necessary for employment, whether that’s a car payment, insurance, or public transit passes

- Health insurance and critical medications that prevent medical emergencies from compounding your financial crisis

Read more: How to Track Your Monthly Expenses: A Complete Guide to Financial Control

Step-by-Step Payment Strategy

Now that you’ve categorized your bills, it’s time to implement a practical payment system. Start by calculating your total monthly income after taxes. Then allocate funds in strict priority order, beginning with Tier 1 and working down only after higher tiers are fully covered.

If you find yourself unable to cover all Tier 1 expenses, you’re basically just one step away from the solution. Contact landlords, utility companies, and lenders immediately. Many offer hardship programs, payment plans, or temporary forbearance. The worst action is silence—creditors can’t help if they don’t know you’re struggling.

Proactive communication often prevents the most severe consequences. You can Leverage 0% APR Balance Transfers: For those with high credit card debt, we basically recommend transferring balances to 0% interest cards to speed up repayment.

The majority of utility companies and creditors now offer hardship programs that prevent service disconnections and protect credit scores, so think about proactively negotiating payment plans before bills become delinquent.

When to Choose Debt Snowball vs Avalanche

For Tier 3 debts like credit cards and medical bills, the debt snowball vs avalanche decision shapes your repayment strategy. The avalanche method targets high-interest debts first, saving the most money mathematically. The snowball method pays off smallest balances first, creating psychological wins that maintain motivation.

Choose the avalanche method if you’re motivated by numbers and want to minimize total interest paid. This approach makes particular sense when you have one or two debts with significantly higher interest rates than the others.

Choose the snowball method if you need the emotional boost of eliminating debts completely, especially if you’re feeling overwhelmed by the number of debts you owe.

| Week | Action Step | Focus Area | Goal |

|---|---|---|---|

| Week 1 | List all bills and income | Complete financial inventory | Know exactly what you owe |

| Week 2 | Categorize by priority tier | Identify critical vs. optional | Create priority debt list |

| Week 3 | Contact creditors for Tier 2-4 | Negotiate payment plans | Secure reduced payments |

| Week 4 | Implement payment schedule | Execute priority-based plan | Maintain Tier 1 coverage |

Read more: How to Live Within Your Means

Common Mistakes to Avoid

Many people sabotage their bill payment strategy through predictable errors. The most damaging mistake is paying bills in the order they arrive rather than by priority. A credit card bill that arrives first doesn’t deserve payment before your rent is due. Always follow your priority debt list, not your mailbox.

Another common error is ignoring creditor communication. When bills go unpaid, many people avoid phone calls and letters from fear or shame. This silence costs money. Creditors who can’t reach you proceed with late fees, collections, and legal action. Those same creditors might have offered payment plans or hardship assistance if contacted early. Your financial situation is business, not personal—treat it that way.

Lastly, avoid using high-interest debt to pay other bills unless you’re facing immediate eviction or utility shutoff. Paying your electric bill with a credit card charging 24% interest just moves the problem to a more expensive place. Explore all other options first: payment plans, hardship programs, community assistance, or temporary work before creating new high-interest debt.

Read more: Best DeFi Wallets Comparison Guide: Features, Types, User Experience, and FAQs

Creating an Emergency Payment Fund

The best way to deal with the stress of paying bills is to have some backup options. An emergency fund changes the game, turning bill payments from a monthly hassle into something you can manage. You don’t need to start big—even putting away $500 can give you some wiggle room for small emergencies that might mess up your payment plans.

Build this fund step by step. After you take care of your must-pay bills (Tier 1) and make the minimum payments on other obligations (Tier 2-3), put any leftover cash into savings. Set this up to happen automatically so you don’t accidentally spend it first. Many employers let you split your paycheck, so you can save without having to do anything extra.

Aim to save enough to cover one month of your essential expenses (Tier 1), and then work up to three months. This safety net means if you lose your income for a bit, you won’t immediately have to worry about paying for your home or utilities. You’ll sleep easier knowing you can handle surprises without having to choose between paying rent or your car bill.

| Milestone | Target Amount | Protection Provided |

|---|---|---|

| Starter Fund | $500-$1,000 | Minor emergencies without new debt |

| One Month Coverage | Tier 1 expenses × 1 | Brief income interruption |

| Three Month Safety Net | Tier 1 expenses × 3 | Job loss, medical leave |

| Full Security | Tier 1 expenses × 6 | Extended unemployment, major setback |

Read more: How to Get Started with DeFi: A Beginner’s Guide to Earning Passive Income

FAQs About How to Pay Off Bills

Here are answers to the most common questions people have when figuring out how to pay off bills smartly.

What if You can’t pay Your Tier 1 bills?

Get in touch with your creditors right away to explain what’s going on and ask about hardship programs. Look for help from local charities, government assistance, or nonprofits. You might also think about quick fixes like borrowing from family or taking on some short-term gig work to help out.

Should I pay bills before buying groceries?

Food is a Tier 1 basic need. Make sure you budget for essential groceries before optional bills, but after housing and utilities. Your minimum food budget should cover what you need to eat, not fancy stuff. Cut back to the basics for a bit while you handle bill priorities.

Is it better to pay bills early or right on the due date?

Pay your Tier 1 bills as soon as you get your income to make sure they’re covered. To build a good payment history and improve your credit utilization ratio, always check these essential financial obligations. For less important bills, paying closer to the due date can help keep your cash flow flexible. This way, you can cover the important bills while still having money for any surprise expenses.

Conclusion

Getting the hang of how to pay off bills by prioritizing them can turn financial stress into something manageable. This guide gives you a clear plan: take care of your essential needs first, then tackle secured debts, followed by unsecured ones, and finally the non-essentials. Your priority debt list will help you navigate both good and tough times.

Just remember that knowing which bills to pay first is just the start. Sticking to these tips, staying in touch with your creditors, and building up an emergency fund will help you stay strong financially. The strategies you’ve learned here can work for anyone, no matter their income. They just need some honest self-evaluation, steady action, and patience.

Get started today by making your full list of bills and a priority debt list. Then follow the four-week action plan to set your payment priorities. Financial stability doesn’t happen overnight, but every month you stick to this system gets you closer to feeling more confident and in control of your finances.

Related Contents

- Debt Snowball vs. Avalanche Method: Which Pays Off Debt Faster?

- How to Create a Debt-Free Budget: 5 Key Strategies

- How to Pay Off Debt Quickly

- A Deep Dive into Secured vs Unsecured Loan

- How to Get Started with DeFi: A Beginner’s Guide to Earning Passive Income

- Best DeFi Wallets Comparison Guide: Features, Types, User Experience, and FAQs

- Basic Financial Concepts You Should Understand

- How to Build Your Reserve Fund: A Step-by-Step Guide for the New Year

- Where to Keep Your Reserve Fund: Best Accounts Compared

- How to Live Within Your Means