Written by: Segun Akomolafe

If you’re searching for the fastest escape route out of debt, you’ve likely encountered two competing strategies: the debt snowball and the debt avalanche. Both promise to eliminate your balances, but they take fundamentally different approaches. One prioritizes psychology, the other mathematics. One celebrates quick wins, the other maximizes savings.

Recent Federal Reserve data shows Americans now carry $1.28 trillion in credit card debt at 22.3% average APR both all-time highs. This is what makes your debt payoff strategy choice more financially critical than ever.

The debate between debt snowball vs. avalanche method isn’t just academic—your choice could mean the difference between paying an extra $2,000 in interest or staying motivated enough to actually finish. Let’s break down both strategies with real numbers, so you can make an informed decision based on your situation.

Quick Answer

The avalanche method for paying off debt usually helps you get out of debt quicker since you focus on the debt with the highest interest rate first, which means you pay less interest overall. On the other hand, the debt snowball method starts with the smallest debts, giving you a boost of motivation with quick wins. The right choice really depends on if you want to save money while paying off debt or if you’d rather be completely free of debt first before saving regularly.

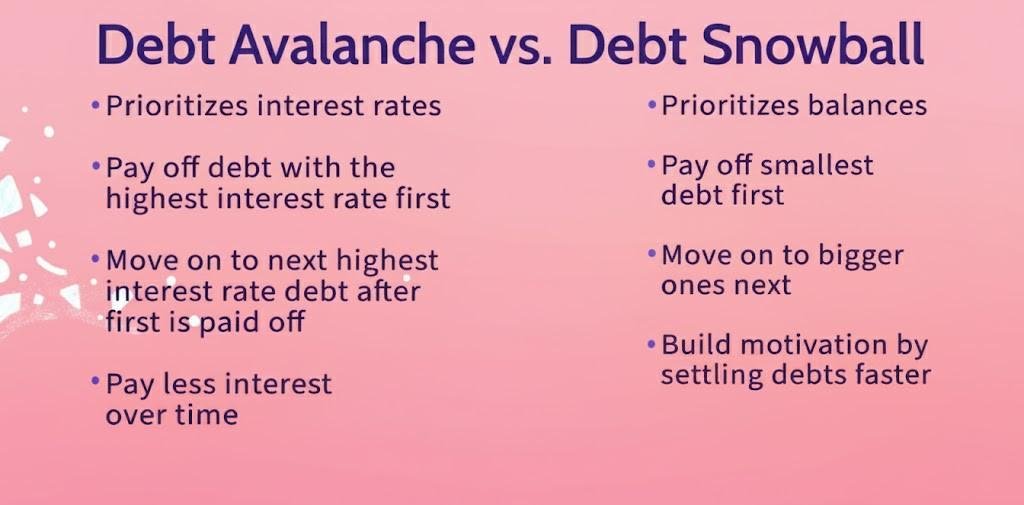

Understanding the Debt Snowball Method

The snowball method attacks your smallest debt balance first, regardless of interest rate. You maintain minimum payments on all debts while throwing every extra dollar at the smallest one. Once that’s eliminated, you roll its entire payment to the next smallest balance, creating a “snowball” effect.

Here’s how it works in practice. Imagine you have four debts:

- Credit Card A: $500 at 22% APR

- Medical Bill: $1,200 at 0% interest

- Credit Card B: $3,000 at 18% APR

- Car Loan: $8,000 at 6% APR

With the snowball method, you’d pay minimums on everything except Credit Card A. Once that $500 disappears—possibly within your first month—you experience an immediate win. That payment now combines with your medical bill payment, accelerating its payoff. The psychological momentum builds as debts disappear from your list one by one.

The strength here isn’t mathematical optimization; it’s human behavior. Research from the Harvard Business Review found that people using the snowball method are 15% more likely to eliminate all their debts compared to those using other strategies. Why? Because seeing accounts close provides tangible proof that the sacrifice is working. The Snowball method helps you with immediate gratification to stay on track.

Read more: How to Pay Off Debt Quickly

Understanding the Debt Avalanche Method

The avalanche method flips the script entirely. Instead of targeting small balances, you attack the highest interest rate first. Minimum payments still cover everything else, but extra funds go toward the debt costing you the most in interest charges.

Using the same four debts from our example:

- Credit Card A: $500 at 22% APR (highest rate)

- Credit Card B: $3,000 at 18% APR

- Car Loan: $8,000 at 6% APR

- Medical Bill: $1,200 at 0% interest

With avalanche, Credit Card A gets your extra payments first because of that 22% interest rate. After it’s gone, you’d tackle Credit Card B at 18%, then the car loan at 6%, and finally the zero-interest medical bill.

The mathematical advantage is undeniable. High-interest debt compounds aggressively—a $3,000 balance at 18% APR costs you $540 annually in interest alone. By eliminating expensive debt first, you can reduce the total interest paid over your debt-free journey. In many cases, this approach saves hundreds or even thousands of dollars compared to snowball.

Financial Efficiency (Avalanche): By prioritizing high-interest debt (e.g., credit cards), you minimize interest charges, allowing more of your payment to reduce the principal, often resulting in a faster total payoff.

Read more: How to Create a Debt-Free Budget: 5 Key Strategies

The Real-World Comparison: Running the Numbers

Let’s test both methods with a realistic scenario. Suppose you have $18,000 in total debt across multiple accounts and can afford $800 monthly toward debt elimination:

- Credit Card 1: $5,000 at 24% APR, $150 minimum

- Credit Card 2: $4,000 at 19% APR, $120 minimum

- Personal Loan: $6,000 at 12% APR, $180 minimum

- Store Card: $3,000 at 15% APR, $90 minimum

- Build payment strategy: Total debt payoff strategy saves thousands in high-interest APR

Snowball Results:

Following smallest-to-largest balances (Store Card → Credit Card 2 → Credit Card 1 → Personal Loan), you’d be debt-free in 28 months and pay approximately $3,850 in total interest.

Avalanche Results:

Following highest-to-lowest rates (Credit Card 1 → Credit Card 2 → Store Card → Personal Loan), you’d be debt-free in 27 months and pay approximately $3,200 in total interest.

Following this avalanche strategy will help you pay off your debts faster and save you a lot of money by lowering your interest costs. The avalanche method saves you $650 and shaves off one month. That’s meaningful money—enough for a car repair emergency fund or a meaningful celebration once you’re debt-free.

However, notice the timeline difference is marginal (one month over more than two years). The snowball method’s first victory happens around month 4 when the Store Card disappears. With avalanche, your first account closure might not happen until month 7, because you’re chipping away at that larger $5,000 balance first.

Read more: A Deep Dive into Secured vs Unsecured Loan

When Debt Snowball vs. Avalanche Method Really Matters

The comparison between debt snowball vs. avalanche method becomes important when you have high interest rate spreads. If your debts range from 6% to 25% APR, avalanche delivers substantial savings. But if your rates cluster between 15-20%, the financial difference shrinks considerably—sometimes to under $200 total.

With the debt snowball method of payment, you see individual accounts reach a low balance much sooner. Harvard research suggests this sense of accomplishment is more likely to keep a person committed until all debt is gone. However, the avalanche method is faster in terms of payment calculation speed.

Recent behavioral studies continue to favor the Debt Snowball for completion. One study indicated that approximately 78% of people using the Snowball method completed their journey, compared to only 52% using the Avalanche method.

Consider your debt profile carefully. Someone with mostly similar interest rates might benefit more from snowball’s motivational structure. Conversely, if you’re paying predatory rates on payday loans (300%+ APR) or high-rate credit cards while also carrying low-rate student loans (4% APR), avalanche isn’t just smarter—it’s dramatically more effective.

Your personality matters too. Are you motivated by spreadsheets showing interest savings, or do you need visible progress markers? Answer honestly. The “best” method is worthless if you abandon it three months in because it doesn’t align with how you stay motivated. Plus, using the snowball method means that getting rid of those smaller debts immediately frees up money each month that can be used to pay for necessities or to pay off the next debt faster.

Is debt snowball or avalanche better for low income?

For low-income earners, the debt snowball method is often better. Eliminating small balances quickly frees up cash flow and builds motivation. By reducing the number of creditors, it simplifies monthly budgeting and reduces anxiety, providing essential psychological wins. When every dollar counts, these quick wins prevent abandonment—making snowball the more sustainable choice despite avalanche’s mathematical advantage.

Read more: How to Improve Your Credit Utilization Ratio?

Which One Should You Pay Back First: Big or Small Debt?

Basically, you should start by repaying a bigger debt at a specific interest rate. However, in practice, it is often easier for people to stay motivated and keep trying to repay their debts when they manage to pay back smaller loans first (Snowball Method), providing quick psychological wins.

The Hybrid Approach Nobody Talks About

You’re not locked into a pure snowball or avalanche. Many successful people use a modified strategy: handle any debt under $500 first (quick psychological win), then switch to avalanche for everything else. This hybrid captures early momentum while maximizing long-term savings.

Early Intervention: The latest trends for the new year show that getting on top of debt payments as soon as possible leads to much better chances of recovering money than just letting the balances get bigger.

Another smart modification: use avalanche but pause every 3-4 months to knock out your smallest remaining balance, regardless of rate. These periodic victories refresh your motivation during the long middle stretch when progress feels slow.

Both strategies can be enhanced by smart budgeting in conjunction with emergency fund building, credit counseling, and debt management plans, which can help achieve financial freedom through disciplined money management.

To temporarily stop interest from accruing on high-rate debt while aggressively paying down principal using either repayment method, take into consideration balance transfer cards with 0% APR promotional periods.

According to recent behavioral finance research, the avalanche method combined with debt snowball method greatly boosts completion rates, thereby bridging the gap between psychological motivation and mathematical efficiency.

The key is intentionality. If you modify the approach, do it strategically—not as an excuse to avoid difficult choices. Make a list of all your debts, then set up automatic minimum payments. Start with accounts that have high interest rates and low balances for quick, satisfying psychological wins.

Read more: 20 Tips For First-Time Home Buyers

Making Your Decision: A Practical Framework

Choose debt avalanche if:

- You have significant interest rate differences (10%+ spread)

- You’re motivated by data and financial optimization

- You’ve successfully completed long-term goals before

- You have high-interest debt above 20% APR

- Saving maximum money is your primary objective

- You possess the discipline to stick with a plan without needing quick emotional wins.

Choose debt snowball if:

- You’ve tried paying off debt before and failed

- You need frequent wins to stay motivated

- Your interest rates are relatively similar

- You feel overwhelmed by the number of debts

- You struggle with financial discipline

Neither choice is wrong. The method you’ll actually follow through on is infinitely better than the “optimal” strategy you abandon. In a typical scenario, a $91,000 debt portfolio took 6 months less to repay using the Debt Avalanche method vs. the Debt Snowball, saving over $6,500 in interest.

As of 2026, with average US debt exceeding $104,000, choosing between Snowball’s motivation and Avalanche’s 20% interest savings is basically critical for payoff. You can go with the quick payment process of the snowball method or the financial savings of the avalanche. The best strategy is to choose the one that works best for you.

Read more: Savings Vs. Investing: Which One Should You Choose?

Your Next Steps

Understanding debt snowball vs. avalanche method intellectually is just the start. Implementation requires three immediate actions:

First, list every debt with its balance, minimum payment, and interest rate. You can’t strategize without complete information. This first step requires going over your credit card statements, loan documents, and unpaid utility bills to find out exactly where your money is going each month.

Second, calculate your available monthly amount for debt beyond minimums. Be realistic—overpromising leads to burnout.

Third, commit to your chosen method for at least six months. Strategy-hopping sabotages both approaches. Pick one, follow it religiously, then evaluate. Set up automatic payments, savings, and progress tracking to make sure you’re consistent, stop spending money because you’re feeling like it, and speed up your journey to being debt-free.

Fourth, visualize your progress and identify small wins. Update a chart, spreadsheet each month to track your balances going down. Recognize milestones (paying off a little credit card, hitting the halfway point) to help you keep your motivation up during the long middle and avoid “debt fatigue”.

The mathematical winner is the avalanche in most scenarios. But debt elimination isn’t purely mathematical—it’s behavioral. If the snowball method keeps you engaged while the avalanche method leads to abandonment, snowball wins decisively. A completed snowball plan beats an abandoned avalanche plan 100% of the time.

It’s not just about math when you choose between debt snowball and avalanche. Choose the one that keeps you motivated, because consistency, not speed, is what will set you free financially.

Automate your debt payments on payday before money sits in checking, removing temptation to spend and ensuring consistent progress toward becoming completely debt-free faster than expected. Simply compare your monthly payment for both the debt snowball and avalanche methods using a free calculator to see which saves you more interest.

Overall, avalanche is superior for total savings, whereas snowball is better for good behavioral motivation. Start by listing all your debts, then ask yourself: do you need quick wins for motivation? If yes, use snowball; if not, use avalanche. Be free to make your choice. Whichever path you choose, start today.

Your debt-free future is built one payment at a time, and the comparing debt snowball vs. avalanche method matters less than consistently executing whichever you select. The best time to begin was yesterday; the second-best time is right now.

Related Contents:

- How to Create a Debt-Free Budget: 5 Key Strategies

- How to Pay Off Debt Quickly

- A Deep Dive into Secured vs Unsecured Loan

- How to Improve Your Credit Utilization Ratio?

- 20 Tips For First-Time Home Buyers

- Savings Vs. Investing: Which One Should You Choose?

- 15 Best Online Banks For Reliable Savings

- Best Bank Bonuses and Promotions in the US

- How to Live Within Your Means